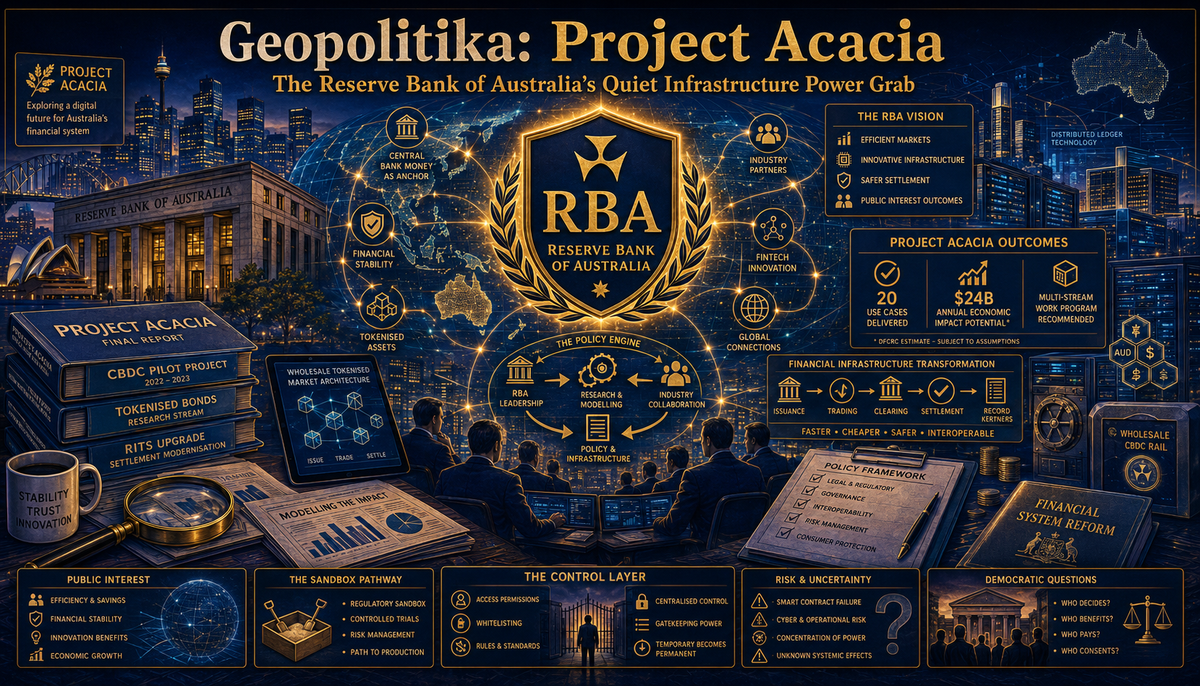

Geopolitika: Project Acacia – The Reserve Bank of Australia’s Quiet Infrastructure Power Grab

This article is published as part of the Geopolitika project to map Anglo-American power structures by examining their founding mythologies, leadership, linkages to power, public face, the nature of their outputs and who these are directed towards. This series is primarily generated from materials provided on the institution’s own websites, which are analysed using a structured analytic framework—see methodology statement at foot of article.

—

Executive Summary

In May 2026, the Reserve Bank of Australia and the Digital Finance Cooperative Research Centre released the final report of Project Acacia—a joint research project exploring how digital money and settlement infrastructure could support wholesale tokenised asset markets. The report describes 20 successful use cases, identifies efficiency gains, and proposes an ambitious multi‑stream work program including a regulatory sandbox, tokenised government bonds, and RITS settlement upgrades.

The stated purpose is neutral exploration. The observable function is not.

Project Acacia is a legitimation device for a specific, RBA‑centred tokenisation pathway. Its design—self‑selected participants, no sceptical institutional voices, pre‑specified workstreams—produces findings that justify continued public‑private investment, expanded RBA authority, and first‑mover advantage for participating banks and fintechs. The $24 billion annual economic gain estimate (DFCRC) figure functions as a rhetorical anchor rather than a rigorously validated forecast—its assumptions are not independently audited in the public report. Lower‑cost, non‑DLT alternatives are mentioned once then deprioritised. Liability for smart contract failure is unassigned. Privacy is not mentioned. Consent is not sought.

This is standard central bank behaviour: convene friendly participants, define the problem narrowly, produce legitimating research, announce workstreams. But standard behaviour does not make it legitimate. The question is not whether tokenisation has potential—it does. The question is: under what rules, for whose benefit, at whose cost, and with whose consent? Project Acacia answers the first three. It does not ask the last.

The Founding Machine: Origins and Core Logic

Project Acacia is the second major RBA‑DFCRC collaboration, following the 2022‑2023 CBDC Pilot Project. Its stated origin is a response to growing global momentum in tokenised finance: Singapore’s Project Guardian, the UK’s Digital Securities Sandbox, Hong Kong’s Project Ensemble. But its real logic is not imitation. It is institutional positioning.

The RBA’s “strategic priority on the future of money” means the RBA wants to remain central as money digitises. Tokenisation threatens that centrality—private stablecoins and decentralised settlement networks could bypass central bank money. Project Acacia’s core logic is to demonstrate that central bank money (either existing Exchange Settlement Account balances or a wholesale CBDC) remains necessary as an “anchor and enabler”. The research question is structured to produce that answer.

The DFCRC, a Cooperative Research Centre funded by government matched with industry contributions, provides the research vehicle. Its industry members include banks and fintechs that participated in the use cases. The production system is not a neutral discovery mechanism. It is a network designed to legitimate a specific policy pathway.

The Authority Engine

Project Acacia claims authority through four channels:

- Central bank authority. The RBA is Australia’s monetary authority. Its involvement signals seriousness, stability, and public interest. But the RBA is also an interested party: expanded settlement authority, whitelisting control over any wholesale CBDC, and a central role in sandbox governance are direct institutional benefits. The report does not disclose this interest.

- Economic modelling. The DFCRC estimates that digital finance innovation could deliver $24 billion in annual economic gains.The figure appears in the media release, executive summary, and main text. A model can usefully warn of coordination barriers and still be too assumption-dependent (full adoption, pass-through to GDP, negligible transition costs) to justify large-scale public investment or regulatory preference without independent validation. Yet the $24 billion figure is used as if it justifies the entire work program.

- Industry consensus. Twenty use cases were developed and tested. Participants included major banks (ANZ, CBA, Westpac, NAB), fintechs, and technology vendors. The report presents their feedback as “industry views”. But participants were self‑selected. No sceptical banks, no consumer advocates, no retail investor representatives, no future‑generation trustees took part. The “industry” in the room was the industry with a vested interest in tokenisation proceeding.

- International precedent. The report cites Singapore, the UK, and Hong Kong as models. This is legitimation by imitation: if other advanced economies are doing it, Australia must follow. But precedent is not justification. Different jurisdictions have different legal systems, political structures, and democratic accountabilities. Copying their policy templates without local democratic debate is not prudence; it is herding.

Together, these four authority channels create a legitimacy cascade: RBA leadership, economic modelling, industry consensus, global best practice. The cascade is designed to make the work program seem inevitable. It is not. It is a choice—and choices require democratic authorisation.

Platform and Translation Power

Project Acacia translates technical feasibility into policy inevitability. It does this through several mechanisms:

- Problem definition. The problem is defined as “coordination failures” and “legal and regulatory uncertainty”. Both are real, but the definition excludes strategic incumbency defence (incumbent banks and settlement operators protecting their revenue streams) and distributional politics (who gains, who pays). A problem defined narrowly produces solutions that fit the definition.

- Solution selection. The favoured solutions are DLT‑based tokenisation, RITS upgrades, and a regulatory sandbox. Lower‑cost, non‑DLT alternatives—extending Austraclear operating hours, improving the New Payments Platform, mandating price transparency without blockchain—are mentioned once (Chapter 1, p.1-2) then deprioritised without published cost‑benefit analysis. This is solution selection bias: capital‑intensive, centralised, expert‑administered pathways are favoured because they create new markets (interchange fees, deposit token custody, synchronisation services) and expand institutional authority.

- Legitimation language. The report uses technocratic, depoliticised language: “coordination challenges”, “interoperability”, “synchronisation mechanisms”. This language erases power, interest, and conflict. It presents policy choices as engineering problems.

- Workstream pre‑specification. Chapter 7 announces a multi‑stream work program: inter‑agency regulator working group, DFMI sandbox, tokenised government bond initiative, extension of the Deposit Token Working Group, RITS consultation, wCBDC research. These are presented as the logical next steps. But they were not derived from the use cases. They were pre‑specified. The exploration was always going to produce this agenda.

Personnel and Networks

Project Acacia’s personnel and network structure reveal its interests.

- Steering Committee: RBA (Brad Jones, Chair), DFCRC (Talis Putnins, Tony Richards), ASIC, APRA, Treasury. Regulators and policy makers, not consumer advocates or civil liberties organisations.

- Industry Advisory Group: Banks, fintechs, DLT vendors, consultancies. No retail investor representatives, no privacy advocates, no non‑participant institutions.

- Deposit Token Working Group: ANZ, CBA, NAB, Westpac, plus DFCRC and regulators as observers. Banks designing deposit token rules, with no non‑bank input.

- Use case participants: Self‑selected. The report does not disclose how many institutions were invited, how many declined, or why. This is not transparency; it is curation.

The network reproduces itself: RBA convenes, DFCRC funds, banks and fintechs participate, regulators observe. Absent constituencies—non‑participant banks, retail investors, future generations, privacy advocates—have no seat at the table. This is not an accident. It is the design.

Funding and Influence Architecture

DFCRC is a Cooperative Research Centre. Its funding model is government matched by industry contributions. The report does not disclose which industry members contributed what amounts. Transparency is partial.

RITS upgrades, sandbox administration, and wCBDC research will be publicly funded. The report does not estimate the cost. It does not ask why taxpayers should subsidise competitive advantage for a subset of financial institutions.

Participating banks funded their own use case development. This is an investment in first‑mover advantage. The report presents this as industry commitment. It is also a barrier to entry: non‑participant banks must now invest to catch up.

The influence architecture is circular: industry funds research (via DFCRC) and use cases; research produces findings that legitimate policy workstreams; workstreams benefit industry participants. The public is not in the loop.

Outputs, Timing and Synchronisation

Project Acacia’s outputs are carefully timed. The final report was released in May 2026, after the 2025‑2026 use case experimentation phase, and before the next federal budget cycle. The media release, in‑brief summary, and final report were published simultaneously, ensuring a coordinated message.

The workstreams are designed to maintain momentum. The DFMI sandbox, tokenised government bond initiative, and DTWG extension are not one‑off projects; they are ongoing processes that will require continued industry engagement and public funding. This is institutional synchronisation: the RBA and DFCRC are not concluding a project; they are launching a permanent agenda.

The Preferred Solutions

Project Acacia promotes a specific set of solutions:

- DLT‑based tokenisation over non‑DLT regulatory reform

- RBA‑anchored settlement (ESA or wCBDC) over purely private stablecoin systems

- Industry interchange utility (AP+ model) over bilateral or decentralised alternatives

- Regulatory sandbox with stage gates over open competition or legislative reform

These solutions share common characteristics: they are capital‑intensive (DLT platforms, RITS upgrades), centralised (RBA authority, scheme operator), proprietary (platform lock‑in), expert‑administered (sandbox gatekeepers), and financeable (interchange fees, public procurement).

Lower‑cost, local, behavioural, decentralised, or non‑market alternatives are not given equal weight. No cost‑benefit analysis compares DLT tokenisation with extended Austraclear hours or better NPP utilisation. The bias is structural: DLT creates new markets; regulatory reform does not.

Who Gains?

Financial beneficiaries (structural, not proof of intent):

- Participating banks (ANZ, CBA, Westpac, NAB): first‑mover advantage in deposit token issuance, interchange fee capture, influence over sandbox design.

- DLT vendors (Fireblocks, Ripple, Hedera, Redbelly): platform lock‑in if their networks become standards.

- AP+: potential scheme operator role for token interchange, collecting fees.

- Consultancies (EY, Allens, Ashurst): implementation work, legal advice, compliance consulting.

Non‑financial gains:

- RBA: expanded authority from RTGS operator to tokenised settlement architect, whitelisting authority for wCBDC, sandbox gatekeeper.

- Participating institutions: policy leverage, regulatory familiarity, competitive advantage over non‑participants.

The report does not disclose these gain pathways. They are emergent properties of the proposed architecture—but they are also predictable. Any serious analysis of tokenisation policy would ask: who stands to benefit? Project Acacia does not.

Private Gains, Public Costs

Private/institutional upside (captured):

- Participant profit

- DLT vendor lock‑in

- RBA authority expansion

- AP+ scheme fees

Public/community downside (socialised):

- RITS upgrade costs: taxpayers.

- Sandbox administration: taxpayers.

- Unassigned liability for smart contract failure: future publics or resolution authorities (Chapter 6, p.47: liability “unclear”).

- Competitive pressure on non‑participant banks: sector instability risk, not modelled.

- No consent mechanism: retail investors, future generations, international investors not consulted.

Asymmetry: Upside captured privately; downside socialised. This is not unique to Project Acacia—it is a standard feature of public‑private infrastructure partnerships—but the report neither acknowledges nor justifies it. It does not ask whether this distribution is fair. It does not ask whether the public would consent if given the choice.

When the Solution Meets the World

Project Acacia’s implementation analysis is confined to normal operation. Failure modes are acknowledged but not assigned.

What gets built: RITS synchronisation layer, DFMI sandbox platform(s), participant DLT nodes, token issuance systems.

What gets governed: Tokenised asset issuance, trading, settlement; interchange between private money tokens; whitelisting for wCBDC.

What breaks under stress (unassigned):

- Smart contract exploit

- Synchronisation operator failure

- Consensus failure on DLT network

- Whitelisting error

- Platform insolvency

- Decommissioning of abandoned DLT platforms

Who cleans up? Not specified. Chapter 6 notes that liability is “unclear where there is no clearly defined administrator”. That means liability defaults to taxpayers, resolution authorities, or future litigation. The cost is deferred, not avoided.

Privacy: Not mentioned. Permanent, immutable transaction records for all wholesale trades—with no right to deletion or anonymisation—are presented as a benefit (“tamper‑resistant records”, “independent auditability”). The trade‑off (commercial confidentiality, right to be forgotten, surveillance risk) is not discussed.

The System Beneath

Project Acacia defends the two‑tier monetary system: central bank money as anchor, commercial bank money for transactions. This is the “system beneath”—the institutional arrangement that the RBA is mandated to preserve.

But tokenisation creates new pressures. Private stablecoins could bypass central bank money. Decentralised settlement networks could operate without RBA anchorage. Project Acacia’s function is to demonstrate that central bank money remains necessary—not because that is an open research question, but because the RBA’s strategic priority depends on it.

The report also defends a specific governance model: expert‑industry coordination with minimal democratic oversight. The workstreams are designed to proceed by regulatory discretion, not legislative authorisation. Parliament may never vote. The public may never be asked. This is the system beneath the system: governance by central bank, regulator, and industry network, with consent assumed rather than sought.

What Is Not Said

Privacy: Privacy is entirely absent from the report. Permanent, immutable transaction records, embedded KYC/AML enforcement in token logic, and RBA-controlled whitelisting and pause powers are presented as unalloyed benefits. The trade-offs—commercial confidentiality, right to be forgotten, risk of erroneous blacklisting, and precedent for programmable money—receive no discussion. This is not a minor technical omission. It is a constitutional silence on the future architecture of financial surveillance and control.

Consent: Not asked. The report does not consult retail investors, non‑participant banks, future generations, or international investors. It does not propose a consent mechanism. It does not acknowledge that consent might be required.

Liability: Not assigned. Smart contract failure, platform insolvency, decommissioning—all unassigned. Chapter 6 notes the gap and moves on.

Lower‑cost alternatives: Not compared. Extending Austraclear hours, better NPP use, transparency mandates—mentioned once, then deprioritised without cost‑benefit analysis.

Distributional effects: Not analysed. The $24 billion estimate models aggregate GDP gains. It does not ask who wins and who loses.

These omissions are not accidental. They are structural to a project that defines its scope as wholesale market efficiency, excluding the distributional politics, privacy trade‑offs, and democratic consent questions that efficiency measures inevitably raise.

The Cracks

Contradiction 1: ESAs can deliver most benefits, yet wCBDC research continues. Chapter 5 states that Exchange Settlement Accounts “cannot deliver the full functionality of an on‑chain wCBDC” but “many of the benefits of tokenisation could still be achieved using ESAs”. If ESAs are sufficient, why continue wCBDC research? The contradiction reveals institutional hedging: ESAs are safe but limit the RBA’s programmability role; wCBDC expands authority but adds risk. The report keeps both options open, but the workstreams favour wCBDC exploration.

Contradiction 2: Warns against walled gardens but proposes RBA‑centric architecture. The report warns against “walled gardens” and emphasises interoperability. Yet its proposed DFMI sandbox and RITS upgrades centre on RBA‑controlled infrastructure. Interoperability is valued until it threatens RBA authority. The openness is conditional.

Contradiction 3: Coordination barrier framed as neutral, but incumbents may lack incentive to engage. The report frames industry coordination as a neutral barrier. But it also notes that “some participants queried whether large incumbents had an incentive to actively engage”. That is not a coordination problem; it is rational rent‑seeking. Incumbents protect their settlement franchises. The report’s solution—sandboxes, RITS upgrades, deposit token working groups—rewards participants and pressures non‑participants. It does not neutralise incumbency; it reorders it.

What It Actually Does

Stated purpose: “Explore how digital money and settlement infrastructure could enhance the functioning of Australia’s wholesale asset markets through the development of tokenised finance.”

Observable outcomes: 20 use cases, pilot wCBDC, Deposit Token Working Group, pre‑specified multi‑stream work program.

De facto purpose: Legitimate and accelerate a specific, RBA‑centred tokenisation pathway, positioning participating institutions as first movers and shaping regulatory conversation before alternatives scale.

Primary function: Signal amplification (of participant interests and RBA strategic priority).

Secondary functions: Boundary maintenance (reaffirming two‑tier monetary system), anticipatory governance (shaping sandbox design, ESA policy, legal finality frameworks), competitive ordering (favouring participants over non‑participants).

The stated purpose is not false. It is incomplete. Exploration occurs, but it occurs within a framework that has already determined the direction of travel.

An Alternative Interpretation

A defender of Project Acacia would argue:

- The efficiency gains from tokenisation are real and substantial.

- Coordination is genuinely difficult; incumbents’ reluctance reflects high switching costs and regulatory uncertainty, not just rent‑seeking.

- Central bank money is necessary for systemic stability; pure private alternatives carry credit and liquidity risk.

- The workstreams are proposals, not commands; they will be subject to further consultation.

- The $24 billion estimate is a research finding, not a policy diktat.

These points are not wrong. Tokenisation does offer efficiency gains. Coordination is difficult. Central bank money does reduce systemic risk. The workstreams are not yet implemented. The $24 billion figure is a model output, not a law.

But the alternative interpretation is incomplete. It does not engage with the selection bias, the pre‑specified workstreams, the deprioritisation of lower‑cost alternatives without analysis, the absence of privacy weighting, the unassigned liability, or the consent gap. A project that systematically excludes sceptical voices, announces its conclusions before independent evaluation, and does not ask affected populations for consent is not “neutral exploration”. It is advocacy dressed as research.

The efficiency gains are real. But how those gains are distributed—who captures them, who pays the costs, who bears the risks, who gets to decide—is a political question. Project Acacia answers the first three. It does not ask the last.

The Stakes: Who Benefits, Who Pays, Who Decides

Who benefits: Participating banks (first‑mover profit), DLT vendors (platform lock‑in), AP+ (scheme fees), RBA (expanded authority).

Who pays: Taxpayers (RITS upgrades, sandbox administration), future publics (unassigned liability), non‑participant banks (competitive pressure), retail investors (no consent).

What is built: Permanent, immutable transaction ledger for all wholesale trades. RBA‑controlled whitelist and freeze powers. Embedded KYC/AML enforcement in token logic. Private synchronisation operators as gatekeepers.

What is not discussed: Privacy. The right to be forgotten. Appeal mechanisms for blacklisting. Democratic oversight of freeze powers. Opt‑out rights for non‑consenting institutions or individuals.

Who decides: The RBA, ASIC, APRA, Treasury, and participating institutions. Not Parliament (no vote required). Not retail investors (not consulted). Not future generations (no representative). Not the public (no consent mechanism).

What is at stake: A constitutional change in the relationship between the state, financial markets, and transactional privacy. The report provides industry coordination, not public consent. Consultation—even if expanded—would not constitute consent. Consent requires binding authorisation or veto power by those who will live with the infrastructure. That mechanism is absent.

Conclusion

Project Acacia is a well‑resourced, professionally executed research project. Its use cases demonstrate real efficiency gains. Its legal analysis is substantive. Its proposed workstreams are internally coherent.

But it is not what it claims to be. It is a legitimation device for a specific, RBA‑centred tokenisation pathway that benefits participating institutions and expands central bank authority, while externalising costs to taxpayers, non‑participant banks, retail investors, and future publics. Privacy is not mentioned. Liability is unassigned. Consent is not sought.

This is not conspiracy. It is standard central bank behaviour: convene friendly participants, define the problem narrowly, produce legitimating research, announce workstreams. But standard behaviour does not make it legitimate.

The question going forward is not whether tokenisation has potential. It does. The question is: under what rules, for whose benefit, at whose cost, and with whose consent? Project Acacia answers the first three. It does not ask the last. Until that question is asked—and answered by those who will be governed, not just those who will gain—the workstreams should not proceed.

Methodology Note: This article is based primarily on documents published by the Reserve Bank of Australia and the Digital Finance Cooperative Research Centre in May 2026: the Project Acacia Final Report, the media release (2026‑13), and the Project Acacia In Brief summary. These materials were examined using a structured analytical framework focused on stated purpose, observable outputs, funding, participant selection, omissions, contradictions, and downstream consequences. Claims about intent are avoided unless directly evidenced. Structural alignment, beneficiary patterns, and recurring outputs are treated as evidence of function, not proof of hidden direction. Where downstream‑power issues are present, beneficiary analysis is treated as structural evidence rather than proof of intent; model uncertainty is distinguished from model invalidity; and model usefulness is distinguished from authority to govern. Public consultation is not treated as public consent; consent requires binding authorisation or veto power, which is absent. The analysis was conducted using a structured institutional analysis framework examining self-presentation, personnel networks, funding architecture, output patterns, synchronisation, contradictions, missing materials, and de facto purpose. All sourced material is publicly accessible. Base analytic outputs are available on request. For methodological details—including Transparency Score definitions, typology classifications, and confidence calibration—see the Geopolitika Series Methodological Statement.

Mindwars Ghosted is an independent platform dedicated to exposing elite coordination and narrative engineering behind modern society. The site has free access and is committed to uncompromising free speech, offering deep dives into the mechanisms of control. Contributions are welcome to help cover the costs of maintaining this unconstrained space for truth and open debate.

If you like and value this work, please Buy Me a Coffee.